Overview

- For Filipino entrepreneurs, business loans can be a powerful tool for growth, but effective management is crucial to avoid financial burden.

- Key strategies include fully understanding loan terms, timely submission of requirements, and budgeting for payments as a top priority.

- Additionally, making more than the minimum payment and establishing an emergency fund can significantly improve cash flow and build strong business credit for long-term success.

Taking out a loan often comes with hesitation for business owners. Cultural perceptions and stories of financial struggles can give borrowing a negative image, especially when applied to business. The fear of debt and repayment challenges may discourage even the most promising ventures from seeking the capital they need.

But when managed wisely, business loans can be a powerful growth tool. With the right strategies in place, borrowing doesn’t have to be a burden—it can become a stepping stone for expansion, stability, and long-term success.

In this article, we’ll walk you through practical, effective ways businesses can manage loans. From planning repayments to maximizing funds, these tips are designed to help you stay in control and make each loan work harder for your business.

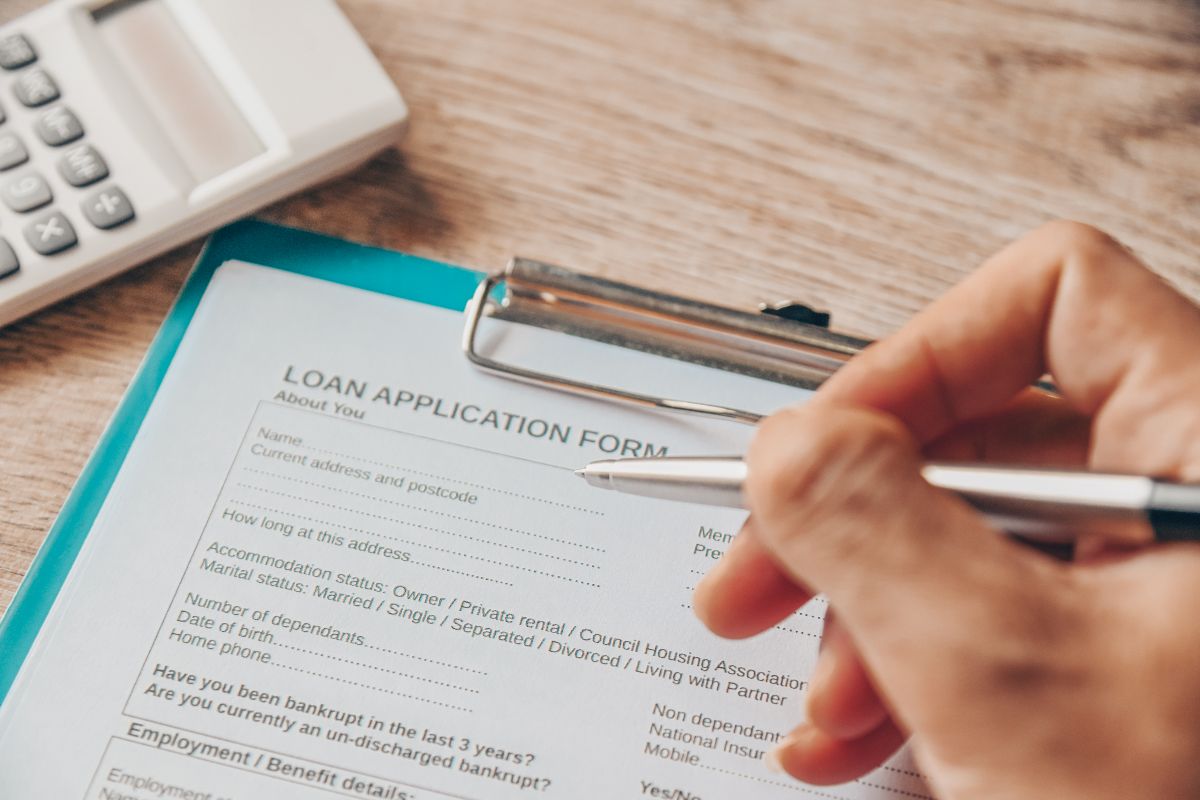

Before committing to any loan, you must understand its terms and conditions. Knowing the original loan amount, interest rate, monthly payment schedule, total repayment period, and any additional fees or penalties is important.

Be aware of the current payoff amount if you decide to settle the loan early. Keeping all this information organized gives you a clear picture of your financial obligations, helping you plan your cash flow effectively.

Take time to carefully read your loan agreement, noting specific clauses that may affect your repayment flexibility or incur extra costs. Don’t hesitate to ask your lender questions—clear communication at the start reduces the risk of misunderstandings later on.

At Bank of Makati, we offer financing options such as SME loans with transparent terms and flexible conditions designed to support your business growth.

Understanding what you’re signing sets the tone for a strong financial partnership and positions your business for more effective loan management.

Consistently tracking your loan covenants and key financial metrics is essential to stay compliant and avoid costly penalties or sudden loan recalls. Setting a regular schedule—whether monthly or quarterly—to review these requirements helps you catch any potential issues early and keep your business on solid financial footing.

Staying informed about any updates or changes to your loan terms can provide opportunities to negotiate better conditions or adjust your repayment strategy. Proactive dialogue fosters trust and can make a significant difference if your business needs flexibility during challenging periods.

Loan covenants may require you to meet specific financial targets, like debt-to-income ratios or liquidity thresholds. Failing to meet these conditions can result in penalties or even loan recall. Regularly checking your compliance status helps protect your access to credit and ensures your loan continues to support your business goals.

Treat loan repayments as a priority expense within your business budget. By setting aside funds for payments before allocating money to less urgent costs, you ensure that your obligations are met consistently and on time. This prevents missed payments that can harm your credit and strain lender relationships.

It’s also important to adjust your budget in response to actual revenue changes. During slower months, trim discretionary spending to protect your ability to cover loan payments. Conversely, when business is booming, consider applying any extra income toward reducing your loan balance faster, saving on interest costs in the long run.

Using detailed cash flow forecasts provides a clear view of upcoming payment requirements, allowing you to plan and avoid unexpected shortfalls. A solid budget helps you handle normal business fluctuations without jeopardizing your repayment schedule.

Paying more than the required monthly amount can significantly accelerate loan repayment. When cash flow permits, allocating extra funds toward the principal helps reduce the overall loan balance faster. This shortens the repayment and lowers the total interest paid over time, freeing up future capital for other business needs.

Strategic overpayments also demonstrate financial discipline, improving your business’s credit profile. Lenders often view proactive repayment behavior as a sign of reliability, which can boost your chances of securing better terms on future loans.

Even small, consistent overpayments can make a difference. Set a goal for additional contributions during high-income months or use seasonal surpluses to make lump-sum payments that chip away at the principal.

While budgeting prepares your business for expected expenses, an emergency fund protects against the unexpected. Economic slowdowns, supply chain disruptions, or personal emergencies can quickly strain a business’s finances. Setting aside an emergency fund or maintaining access to a backup credit line is essential. These reserves provide a safety net to ensure loan payments remain on track even during tough times.

Consistent repayment protects your business’s credit standing and prevents additional costs from late fees or penalties. It also signals financial responsibility to lenders, which can be valuable when applying for future funding.

To support timely payments, consider automating loan deductions from a designated account. This streamlines the process but also helps maintain a reliable repayment history regardless of external circumstances.

Taking out a loan for your business does not have to be a daunting task. By knowing the various ways businesses can effectively manage loans, you can find the right strategy for your enterprise.

Help your business grow with Bank of Makati. We offer comprehensive financial solutions and expert advice designed to support your vision and fuel your expansion. Contact us today to learn more!